There's Money in Them Thar Roth Conversions

MaxiFi's Roth Conversion Optimizer Is a Must Try

MaxiFi Premium costs $149. Since we integrated MaxiFi’s Roth Conversion Optimizer in MaxiFi, I’ve yet to run a conversion case that didn’t produce massive multiples of $149 via savings in federal and state income and Medicare Part B IRMAA taxes. In the case I presented here, the Conversion Optimizer produced $147,837 in present value lifetime tax savings, which is 992 times $149! And that’s just the gains from Roth conversions!

Let me take you through another Roth conversion case. The gains are smaller, but still huge. But before I do, here’s the back story for those new to Economics Matters and my occasional personal finance newsletters and podcasts based on MaxiFi Planner, my company’s economics-based, lifetime financial planning software.

If this sounds like a sales pitch, it is. But it’s from someone who has spent over three decades building the best financial tool going. I did so for two reasons — to help people from all walks of life get responsible, economics-based guidance on improving their finances and to produce state-of-the-art economics research on topics ranging from inequality to work and saving disincentives to the lifetime benefit increases people can achieve from optimizing Social Security. I work for my company for nada — not a penny and always have. I’m well paid by Boston University and prefer to pay back — to society, by keeping our prices extremely low and to my amazing colleagues. Hence, please believe what you read. It’s written to make you, not me, financially better off.

MaxiFi — a Quick Overview

Unlike conventional financial planning tools, MaxiFi doesn’t ask you what you’d like to spend. Instead, it calculates what you can afford to spend on an ongoing basis. Specifically, it figures out how much you need to save (i.e., not spend) to safely sustain your household’s living standard — its discretionary spending per household member with adjustments for economies of shared living and the relative costs of children. Economists call this consumption smoothing.

MaxiFi takes into account all your economic resources as well as your fixed/required spending — your need to pay housing costs, taxes, alimony, and other off-the-top expenses. The tool makes extremely precise annual tax and Social Security benefit calculations and does so inside a second. This is astonishing given that MaxiFi’s algorithm must handle a highly complex simultaneity problem and respect cash-flow constraints. The simultaneity problem references the fact that a household’s sustainable spending depends on its future tax payments and life insurance premium payments. But a household’s future tax payments and premiums depend on the its sustainable spending path.

MaxiFi uses advanced algorithms to solve this problem. And, no, AI will never get this right given that it’s being trained on the wrong answers. More fundamentally, when it comes to personal finance, you need the precisely correct answer, not an answer that’s guaranteed to be precisely wrong for a simple reason — it’s based on prediction, not computation and, again, trained to predict the wrong answers.

Consumption smoothing also requires holding the right amount of life insurance to ensure potential survivors have, if the case of early death, the same living standard they would otherwise have enjoyed. MaxiFi calculates this as well. In addition, MaxiFi finds safe ways to raise your lifetime Social Security benefits and lower your lifetime taxes, including via MaxiFi’s Roth Conversion Optimizer.

As for risky investing, MaxiFi provides two analyses. First, it shows you how to invest in the market without putting your basic living standard at risk. The key is investing in a TIPS ladder to secure your living standard floor and spending out of risky assets only when they’ve been made safe, i.e., converted to TIPS. We call this Upside Investing because you face only the “risk” of a higher living standard floor.

Second, MaxiFi’s Full Risk Investing shows the range of downside as well as upside living-standard outcomes you can experience from not just investing in risky assets, but also spending out of risky assets — spending that may, ex post, have been too high because it was predicated on those risky assets performing well, not going down the tubes.

Full Risk Investing also helps you consider, based on your risk tolerance, how to invest now and over time. The analysis here is based on economics’ lifetime Expected Utility Maximization, developed by the great physicist, John von Neumann and economist, Oscar Morgenstern. (Btw, von Neumann played a critical role in developing the atomic bomb.)

For finance nerds, the seminal analyses of optimal portfolio choice by Markowitz, Sharpe, Tobin, and Merton, each of whom received the Nobel Prize in Economics, was based on Expected Utility Maximization. So is virtually all of the field of modern finance. Every student in every finance department in every top business school in the country is taught Expected Utility Maximization on day one. The same goes for economics PhD students at all leading economics departments. MaxiFi’s Full Risk Investing is the only software program that implements Expected Lifetime Utility Maximization and does so on a lifetime basis taking precise account of federal and state taxes, FICA taxes, all Social Security benefits, and Medicare Part B IRMAA premiums (taxes).

With this background, let me turn to this newsletter’s main objective:

Providing Another MaxiFi Roth Conversion Optimizer Example

Morgan and Jenn, who I featured here, are a Connecticut couple in financial trouble. They are in their mid fifties, make a combined $325K a year, but have saved far too little to maintain their current lifestyle. Yes, they have $1.5 million in retirement accounts, but they want to retire at 62 and immediately take Social Security. Plus, they are house poor. They have a $1.5 million home with a $500K mortgage. Their property taxes, insurance, and other housing expenses total $30K a year. And, they are saving nothing apart from contributing to their 401(k) accounts.

Rescuing Morgan and Jenn’s Retirement

As MaxiFi shows, Morgan and Jenn’s affordable present value of lifetime discretionary spending is $2.5 million. That sounds like a lot. But it entails, leaving aside caring for their two teenagers, annual sustainable spending of $77K per year in today’s dollars. That’s a far cry from the $120K per year that Morgan and Jenn are currently spending!

Let me use MaxiFi to rescue Morgan and Jenn’s retirement. I’ll do so by changing their plan on a step-by-step basis and then add icing to the cake using MaxiFi’s Roth Conversion Optimizer. Here’s the breakdown of increases in lifetime spending, where I add each change to their plan on top of the prior changes.

Work till 65 and take Social Security at 65 — $589,118 increase!

Move to Tennessee when Morgan reaches 65 — $46,086 increase!

Downsize to a $500,000 house in TN purchased with cash — $1,080,345 increase!

Take Social Security at 70, not 65 — $176,772 increase!

Start smooth retirement account withdrawals at 70, not 65 — $49,934 increase!

Optimize Roth conversions — $45,892 increase!

The couple’s optimal Roth conversions entail converting almost one third of their retirement accounts, but doing so gradually over the next 15 years. And the pattern is anything but smooth. For Morgan, the largest conversion — $50,044 — occurs this year. The smallest — $457 (in today’s dollars) — occurs in 2033. For Jenn, the largest conversion — $27,837 — also occurs this year and the smallest — $254 — also occurs in 2033. But for both spouses, most conversion years entail amounts above or well above $10,000.

MaxiFi to the Rescue

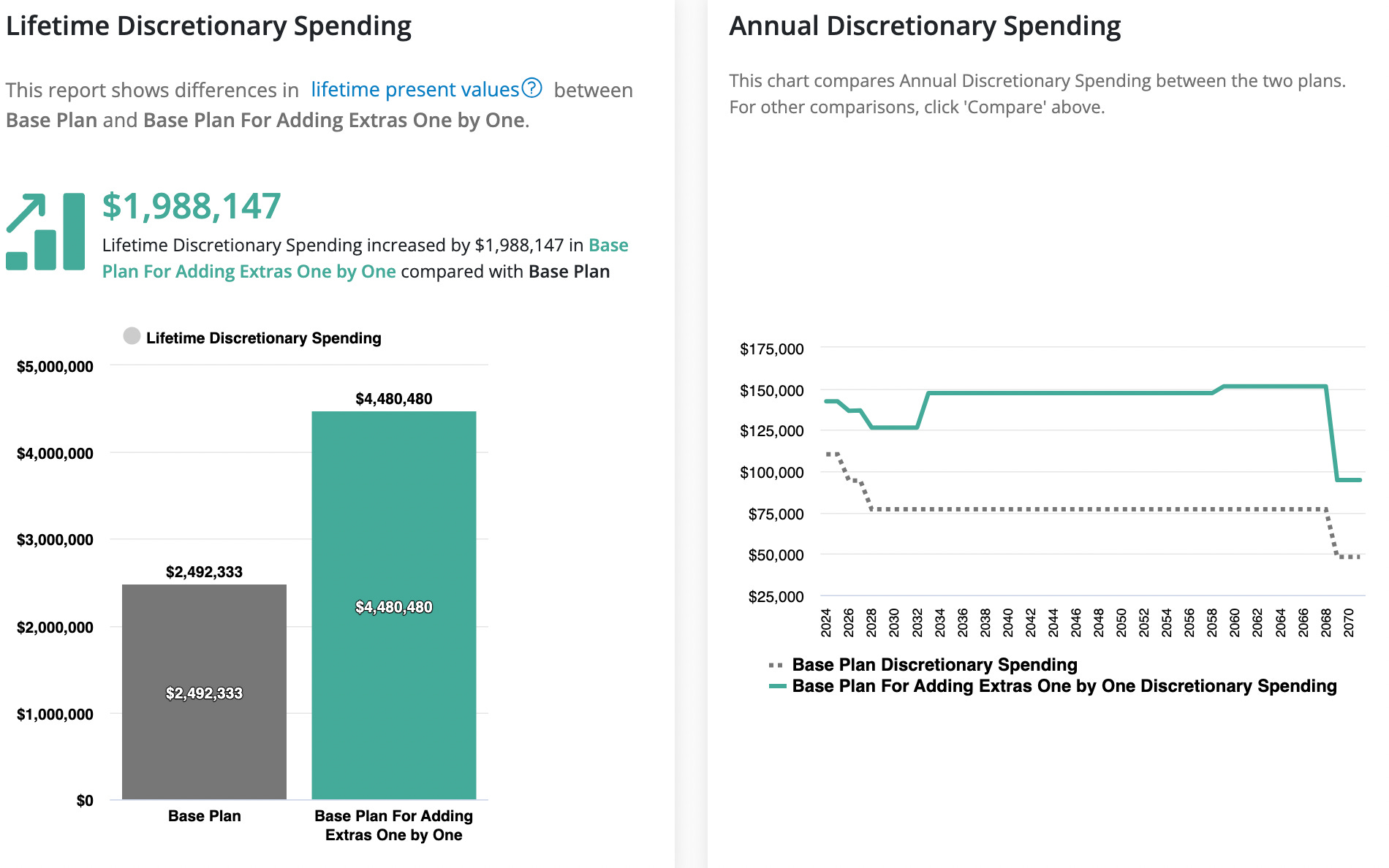

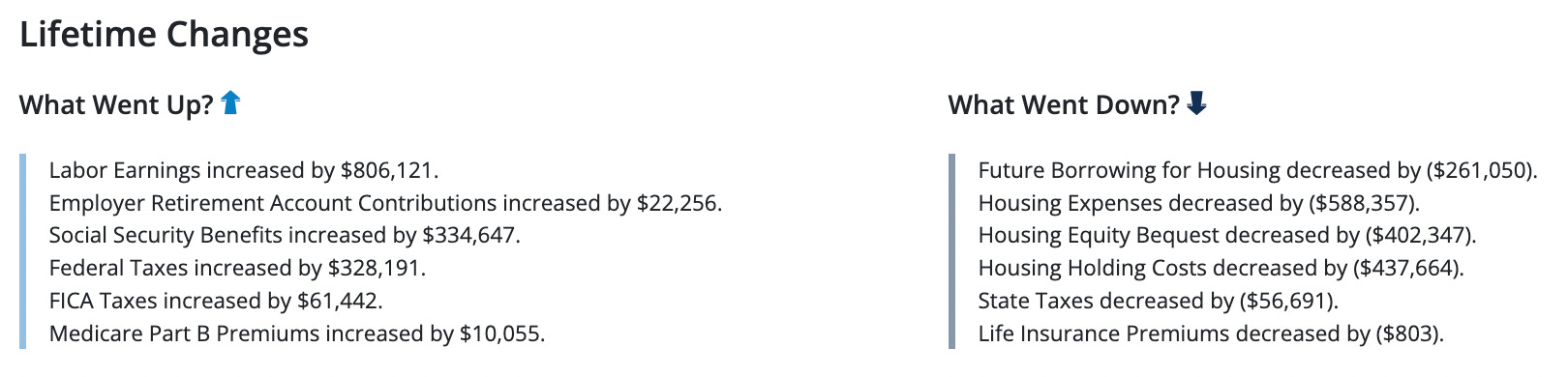

The combined impact of these Maxifications is shown in the charts below. As the left-hand chart indicates, MaxiFi raised Morgan and Jenn’s lifetime discretionary spending by 80 percent! The second chart shows the changes, in present value, in specific components of the couple’s lifetime resources and fixed (non-discretionary spending) that permit a whopping $1,988,147 increase in the present value of the couple’s remaining lifetime discretionary spending.

Indeed, as the right-hand-side chart’s green curve shows, the couple’s annual discretionary spending, with all changes included, exceeds what they could sustainably spend in their base plan (the dotted curve). It even exceeds their current excessive level of spending. Both curves drop as the couple’s two teenagers leave the household and when Morgan reaches his maximum age of life. The green curve jumps up when Morgan reaches 70 — when his Social Security and retirement account withdrawals begin. Prior to that year, the couple is cash-flow constrained.

Note that the Roth conversion gain of $45,892 is 308 times the $149 cost of MaxiFi Premium. The overall $1,988,147 gain is 13,343 times the program’s cost!

The Gains from Roth Conversions Depend On Your Other Moves

What if Morgan and Jenn stick to their original plan. How much can Roth conversions help? The answer is $22,851. That’s still 153 times the cost of the tool. But it’s only about half of the conversion gains when the other five changes are undertaken. Hence, I recommend running MaxiFi’s Conversion Optimizer — Just click the Maximize report and then select Optimize Roth Conversions — after you’ve incorporated everything you want to include in the profile you’re considering.

If You Don’t Fancy Running Software

We’ve had tens of thousands of people run MaxiFi Planner over the years. It’s very user-friendly and we have an extensive Learning Center and great customer support that you can access by clicking on the green help icon at the bottom right of every MaxiFi screen. Still, you may not be keen on doing your own financial analysis. In this case, you can use our co-piloting service with PhD economist and CFP, Jay Abolofia, or have me run your plan.

If you’re using a financial planner, they can buy a professional license and run your plan for you. If your planner doesn’t want to do economics-based planning or is restricted to using another tool by his home office, here are advisors using MaxiFi. Alternatively, you can run MaxiFi and show the results to your advisor.

Don’t Get Addicted

Finding safe ways to raise your living standard can be more addictive than playing video games or surfing the web. The last time I worked on Morgan and Jenn’s plan, I raised their lifetime spending by 69 percent. This time, with the help of MaxiFi’s new Roth converter, I reached 80 percent.

Part of the fun is figuring out why the program comes up with its answers. Step 5 of the six steps surprised me. But then I looked at the program’s detailed reports and things became clear. In selling their Connecticut home, Morgan and Jenn end up with significant additional regular assets and, thus, regular asset income. This pushes them into higher federal, state, IRMAA, and taxable Social Security benefits tax brackets. (CT’s state income tax has, btw, has, like the federal income tax, seven tax brackets!) Taking their retirement account withdrawals before 70 exacerbates this problem of higher tax brackets. With more time, I’m sure I could have tweaked the couple’s gain to at least 85 percent. I was tempted to keep at it, but figured 80 percent was enough to get you to give MaxiFi a try if you haven’t already.